Our dear politicians who want to reindustrialise Europe should keep the automotive bird in their hands rather than looking for two defense ones in the bush

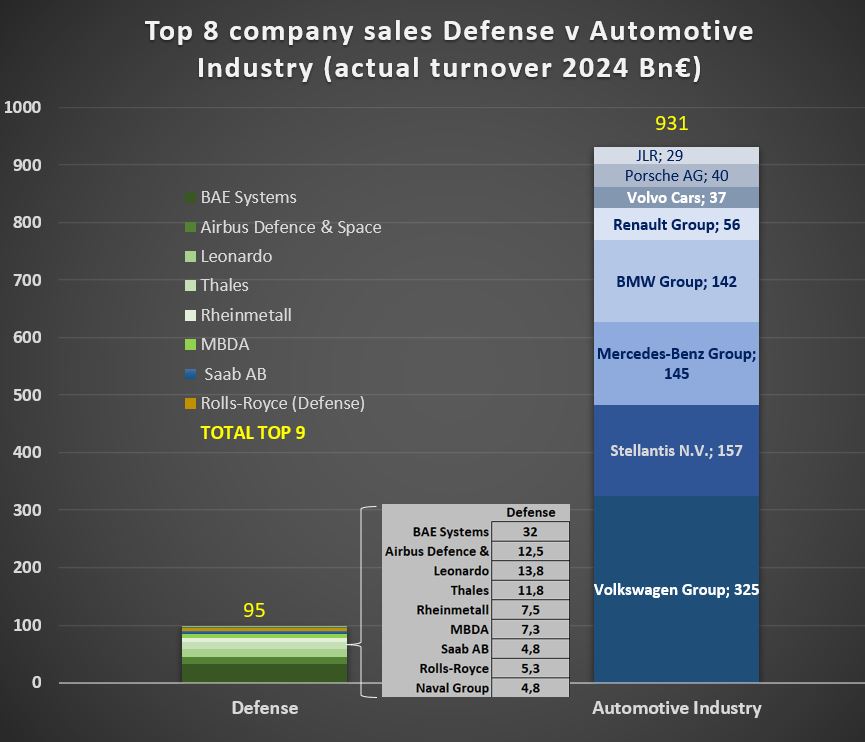

Although I appreciate that this is a bit of peers and apples, the graph below showing turnover of Top 8 companies in each industry makes the point that automotive industry is still a giant compared to defense.

As you can find in the ACEA (European Automotive Association) guide book automotive represents more than 15 millions jobs, making by far the biggest one in Europe.

Numbers below are total turnover including European domestic sales and export.

Eg. BMW numbers include cars made in USA and / or sold in USA. Same applies for Thales or BAE which also make a big part of their turnover outside Europe.

True defense companies turnovers are growing when automotive ones are flat-ish. Defense industries will grow thanks to European order books but considering that export will grow less if not decrease in a more and more regional world, even a doubling of European orders should not lead to a doubling of the total sales.

Hence it would still remain small compared to automotive and could no way compensate for the decline of automotive as some journlist hint it could do.

It is interesting to note that the « famous » French Dassault Aviation is not even in the list. It makes approx. 6Bn€ of sales out of which the Rafale makes about 4Bn€. Source Dassault System.

Maybe a reason why his CEO should be a bit more humble when it comes to the SCAF program and (re)engage into a true cooperation with Germany and others.

Also good for the general public to know that the majority of the order book since the launch of the Rafale (past and future) has been for export, with barely 200 planes expect to join the French air force and navy across more than 30 years. This is on average less than 8 per year.

And good to also have in mind that the future order books for French Air Force is only 45 units, not a single more than what was planned 5 or 10 years ago. Just for those who talk of increasing production. No need to increase for France, no additional orders have been placed. 3/4 of production yet to be done is for export outside Europe.

The myth that Rafale production is increasing for France is… a myth!

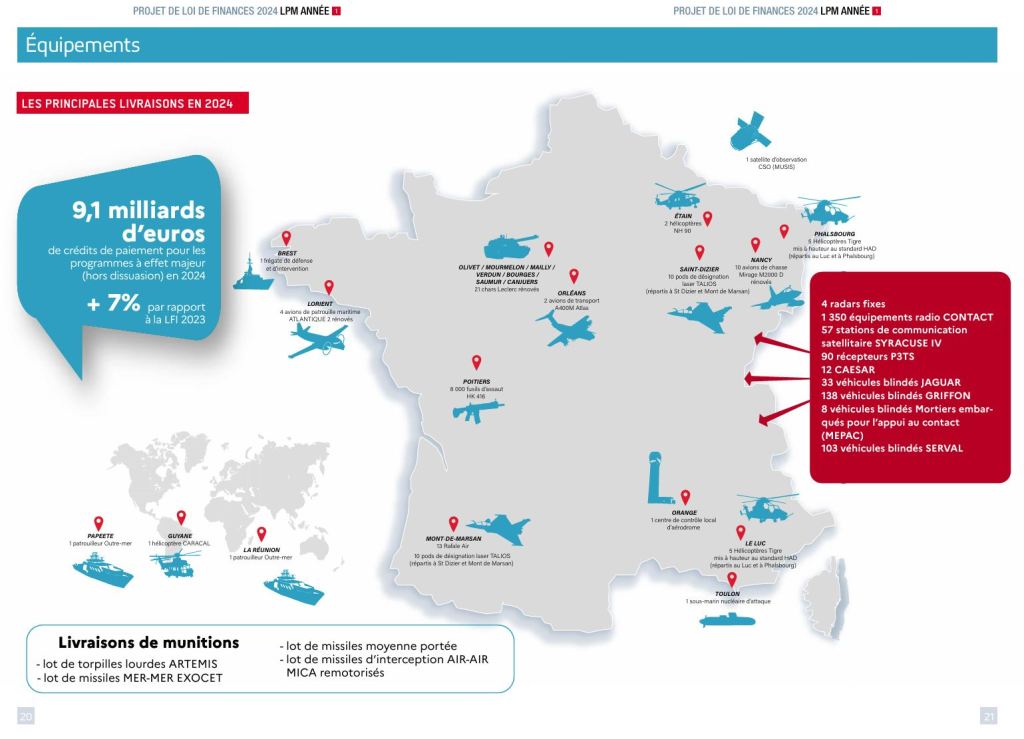

To give another idea, let’s look at numbers of equipment delivered, military vs civilians.

Below slide shows (expected) deliveries of main military equipments in France in 2024.

Looking at land vehicles for instance, the plan was to have 282 armored wheeled vehicles delivered.

By comparison approximately 50,000 trucks have been registered in France during the same period.

So even if I a appreciate that a military truck is a more complex thing, as it needs to be armored, to be equiped with lot of electronic etc. this is still a 1 to 177 ratio.

Find below links to the ACEA « facts and figures », reminding us for instance that automotive in Europe is 13.6 millions jobs and 6.9% of employment?

https://www.acea.auto/nav/?content=facts

https://www.acea.auto/publication/the-automobile-industry-pocket-guide-2025-2026/

Likewise the delivery of 13 Rafale and 2 A400M planes can be compared with the shipment of 766 Airbus during the same period. Agree it’s not the same scope – France v global – yet it gives an idea of how small the military is compared to civilian.

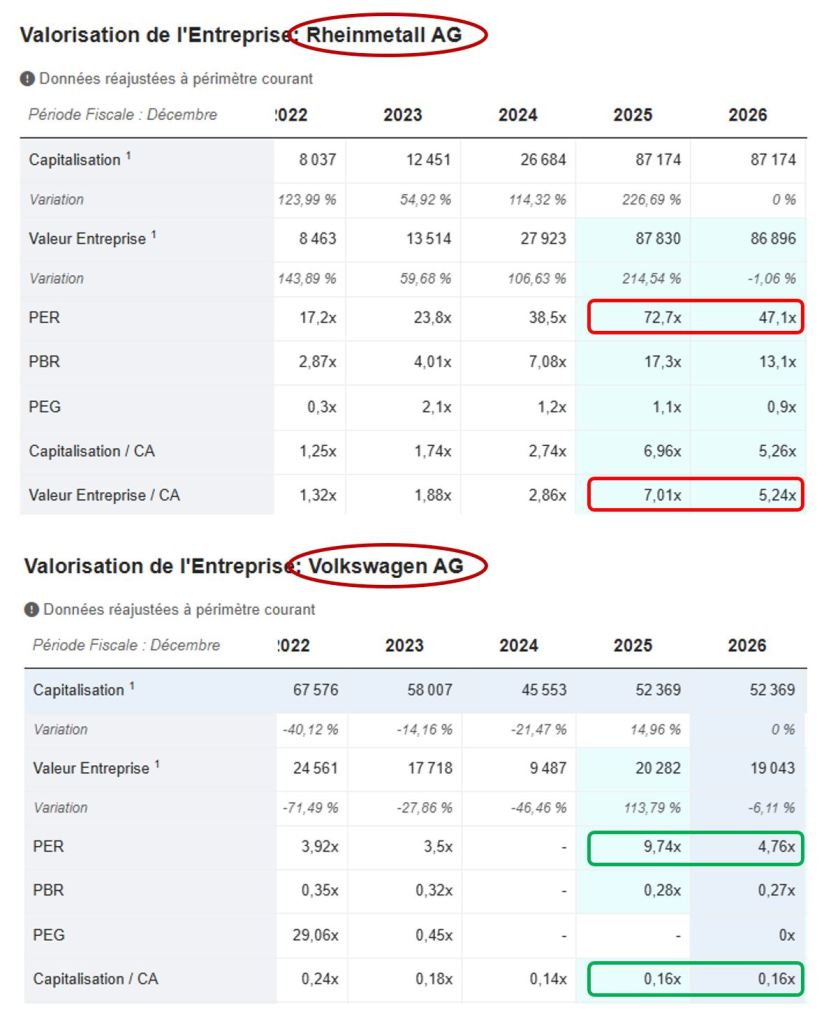

Yet market capitalisations seem to reflect hopes that the trees will reach the sky

I’m not a financial analyst, barely a small individual investor. Hence my point is not to give any advice to whomever on this field.

Yet striking to see the PER (Price Earning Ratio ie ratio between value of a company and its actual or expected profits) of 5 to 10 for automotive vs 40 to 60 for defense.

Sales growth is one thing, profitability is another one. Hopefully one day the bureaucratic procurement teams of the different armies in Europe will start doing their job and push for decent price.

Even Trump reacted against excessive costs charged to the armies. It needs to change also in Europe.

There is no such good thing as competition (and such bad one as national monopolies).

In conclusion my point is not to criticize defense industry. They do what they are asked to do and there is no reason why they would produce kits without purchase orders.

There is also no reason why they would invest in increasing production capacities when their main customers, the European states, do not provide visibility and do not commit on multi-year programs.

Some countries like Sweden, the Nordics, do a good job to provide multi-year visibility and push for « On Time Delivery at Competitive Cost« . Some others like the Club Med are still at the beach…

For sure there is massive room for improvement in term of costs and efficiency. And lead times.A healhy pressure needs to be put to get best value for tax payers money

Yet, all in all, even with ~25% of 3% of defense budget put on equipment and R&D (NATO recommendation is > 20%) this will only be a small % of GDP or so vs 7% or so for automotive.

We all need to keep these ratios in mind when defining industrial policies and when investing our own money!

Return to main page: France, Europe Réagir

To go further:

The Economist October 29th 2025: Europe’s defence firms are flying. Now for the hard part

Valuations have surged since Donald Trump’s return. Are investors heading for disappointment?

https://www.economist.com/business/2025/10/29/europes-defence-firms-are-flying-now-for-the-hard-part

The Economist September 18th 2025: Dodgy defence maths conquers in Europe, The weird and wonderful calculations behind the 5% target

https://www.economist.com/europe/2025/09/18/dodgy-defence-maths-conquers-in-europe

Laisser un commentaire